Continental Disconnect: Why Europe's DNVB Hopes Remain Elusive

Despite a vibrant e-commerce landscape and sophisticated consumer bases, direct-to-consumer brands originating in Europe have struggled to achieve the scale and market penetration seen in North America, facing unique structural and cultural impediments.

While Berlin's Gorillas and its rapid grocery delivery peers burned through substantial venture capital before consolidating or retrenching, their trajectory offered a stark reminder of the hurdles facing digitally native vertical brands (DNVBs) in continental Europe. Unlike their predecessors in North America, which often achieved widespread consumer recognition and significant valuations, many European DNVBs have found scaling beyond their initial niche challenging, even within the burgeoning digital economy.

The initial promise of bypassing traditional retail channels and fostering direct customer relationships remains compelling. However, the fragmented nature of the European market, characterised by distinct national consumer preferences, regulatory frameworks, and logistics infrastructures, presents a formidable barrier. A DNVB successful in France, for instance, cannot simply replicate its playbook in Germany or Italy without significant adaptation. This complexity stands in contrast to the comparatively homogenous market of the United States.

Cross-Border Complexities and Local Giants

Navigating an array of languages, payment methods, and national consumer protection laws complicates pan-European expansion. Shipping across borders from a central warehouse introduces customs delays and increased costs, negating some of the operational efficiencies DNVBs seek. This environment disproportionately benefits established e-commerce giants like Zalando, whose robust cross-border logistics and localised marketing cater to diverse European preferences. Similarly, national champions such as Allegro in Poland or Bol in the Netherlands maintain strong domestic footholds, leveraging existing brand trust and fulfilment networks.

Traditional retailers are also not passive observers. Carrefour and REWE, for example, have invested heavily in their own digital capabilities and sophisticated online grocery delivery systems, often leveraging their extensive physical store networks for last-mile fulfilment. This hybrid approach allows them to offer speed and convenience that pure-play DNVBs struggle to match without substantial infrastructure investment.

The notion of a singular 'European consumer' remains largely theoretical for DNVB strategists; successful market entry demands granular understanding of each national psychology.

Further complicating matters is the strong preference for local brands in many categories, particularly within food and household goods. While a DNVB might carve out a niche for ethical skincare in Sweden, penetrating the broader French cosmetic market, dominated by heritage brands with generations of trust, proves an entirely different proposition. Even in fashion, where platforms like Vinted demonstrate the appetite for thrifting and novelty, scaling a new apparel DNVB to rival established brands or the offerings of large marketplaces remains an uphill battle.

Capital Constraints and Exit Paths

The funding environment also plays a role. While European venture capital has grown, the cheques written for growth-stage DNVBs often fall short of the sums available in Silicon Valley, limiting aggressive expansion strategies. The path to profitability is therefore under greater scrutiny from investors, pressuring DNVBs to demonstrate strong unit economics early. Exit opportunities, too, appear more limited. Acquisitions by larger conglomerates or IPOs have been less frequent for European DNVBs of significant scale compared to their North American counterparts.

The enduring challenge for European DNVBs is to reconcile the promise of digital-first customer engagement with the persistent realities of a continent that, for all its economic integration, remains distinct in its consumer habits and commercial landscapes. Success demands not just innovation in product or marketing, but a sophisticated, adaptive strategy that acknowledges and overcomes these ingrained structural differences.

News Legacy maintains editorial independence. Some recommendations may contain affiliate links. We earn from qualifying purchases at no additional cost to you. Read our policy.

Read Next

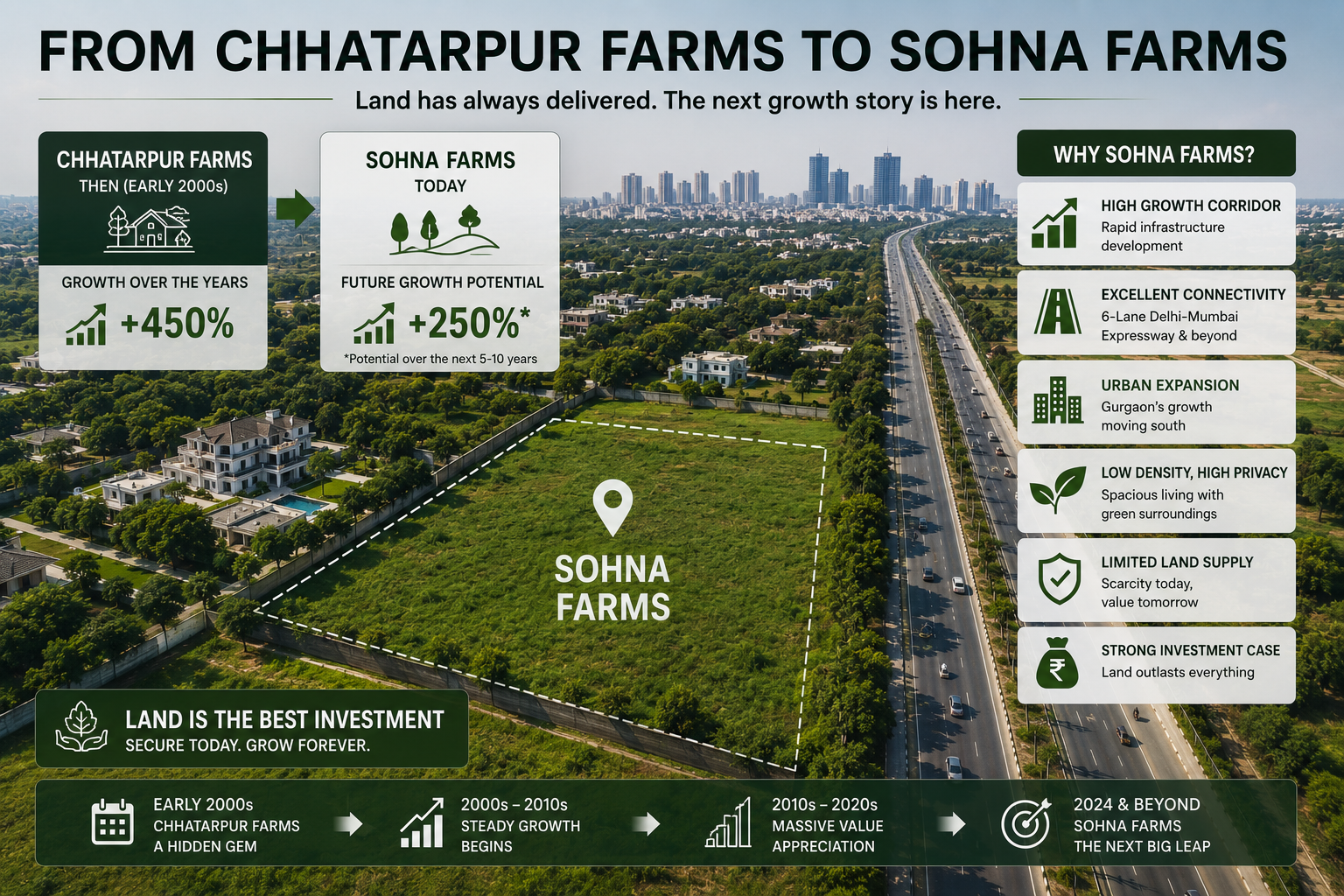

Is Sohna Really the Next Chhatarpur?

Three decades after Chhatarpur redrew South Delhi's map for space, privacy and exclusivity, a familiar pattern is now taking shape further south, and Sohna is where the smart money is beginning to look.

How Chhatarpur Farmhouses Created Multi-Crore Wealth for Early Buyers

What a quiet corner of South Delhi can teach investors about land, scarcity, and long-term wealth creation.

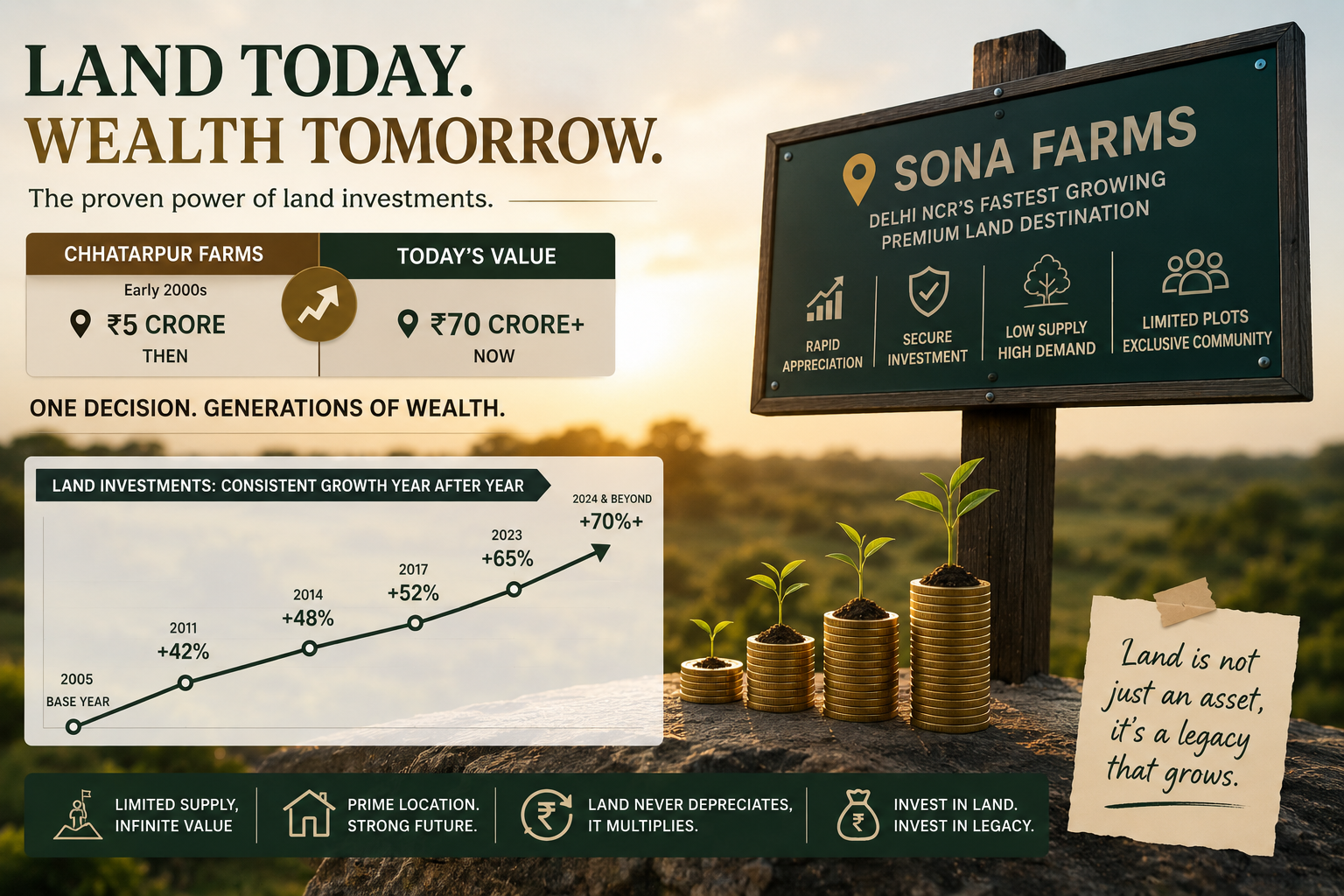

The ₹5 Crore Land Purchase That Became Worth ₹70 Crore

What the Story of DLF Chhatarpur Farms Reveals About Wealth Creation Through Premium Land Ownership

One short email. Stories you can use.

A free, occasional email from our editorial team with our latest features, explainers and reads. Unsubscribe any time — your email stays with us.