Continental Disruption: The Enduring Challenge for Europe's DTC Aspirants

Despite a vibrant start, many direct-to-consumer brands across Europe continue to grapple with the complexities of scaling beyond initial market penetration, confronting entrenched incumbents and fragmented logistics.

In the bustling consumer landscape of Berlin, a local artisan coffee subscription service, once a darling of venture capital, recently announced its cessation of operations. Its plight is far from isolated; across Europe, direct-to-consumer (DTC) brands, initially lauded for their agile direct-to-consumer model and digital native approach, are confronting the harsh realities of sustained growth. The narrative that prioritised brand-building over foundational infrastructure is proving unsustainable for many as they attempt to transition from niche players to significant market forces.

The European market, while offering considerable scale, presents a unique set of hurdles. Linguistic diversity, varying consumer preferences, and especially the intricate web of cross-border logistics and regulatory frameworks, create a formidable barrier to expansion. A brand excelling in France, for instance, might find its distribution model unviable or immensely costly when attempting to reach customers in Poland or the Nordic states. This fragmentation often dilutes the economies of scale that DTC models are theoretically designed to leverage.

The Incubent Advantage and Marketplaces

Traditional European retail giants and burgeoning marketplaces are further complicating the DTC trajectory. Players like Zalando in fashion, or Bol.com and Allegro in general merchandise, offer established infrastructure, vast customer bases, and often superior delivery networks. For a burgeoning DTC clothing brand, the cost of acquiring a customer directly across multiple European countries can quickly outstrip the margins available, making an Amazon or Zalando storefront a more pragmatic, albeit brand-diluting, proposition.

The grocery sector is another battleground. While innovative services like the now-defunct Gorillas and Flink attempted to disrupt rapid delivery, the enduring strength of Carrefour, REWE, and Lidl, with their immense physical footprints and established supply chains, remains paramount. These retailers are not static; they are actively investing in their own e-commerce and last-mile capabilities, further squeezing the space for pure-play DTC grocery ventures.

The allure of maintaining direct customer relationships must be critically weighed against the prohibitive cost of building a competitive, continent-wide fulfilment and marketing apparatus from the ground up.

Scaling Logistics and Trust

Beyond marketing, the logistical challenge is severe. Delivering a custom-blended tea to a customer in Spain from a hub in Germany requires navigating customs, differing postal services, and competitive shipping rates that often favour high-volume established players. This complexity directly impacts the customer experience, an area where DTC brands are meant to excel. Delayed deliveries, unexpected import duties, or difficult returns can erode the trust painstakingly built through sophisticated branding.

Even successful pan-European platforms like Vinted, which facilitates second-hand fashion exchanges, highlight the power of network effects and critical mass in overcoming some of these cross-border complexities by decentralising aspects of the transaction. For individual DTC brands, replicating such infrastructure independently is often financially untenable, diverting precious capital from product development or brand narrative.

Ultimately, the European DTC market is maturing. The initial wave of brands that focused primarily on digital marketing and compelling narratives are now confronting the unglamorous but vital tasks of operational excellence, pan-European logistics, and efficient customer acquisition across disparate markets. Those that can integrate these elements effectively, or strategically partner with existing platforms, will be the ones that endure and thrive in a market valued at hundreds of billions of euros annually. The romantic notion of bypassing intermediaries has collided with complex commercial realities, compelling a more nuanced and strategic approach to growth.

News Legacy maintains editorial independence. Some recommendations may contain affiliate links. We earn from qualifying purchases at no additional cost to you. Read our policy.

Read Next

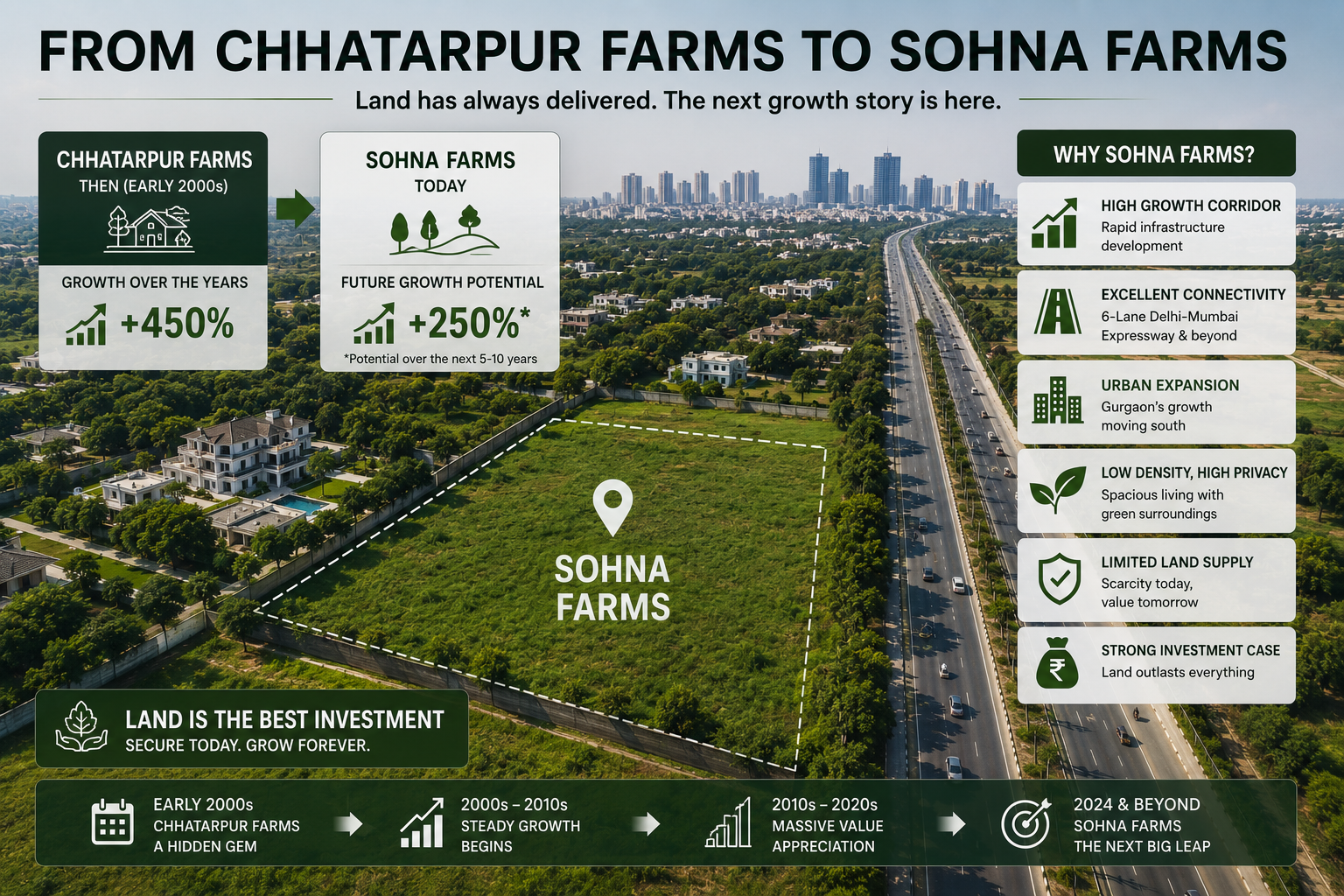

Is Sohna Really the Next Chhatarpur?

Three decades after Chhatarpur redrew South Delhi's map for space, privacy and exclusivity, a familiar pattern is now taking shape further south, and Sohna is where the smart money is beginning to look.

How Chhatarpur Farmhouses Created Multi-Crore Wealth for Early Buyers

What a quiet corner of South Delhi can teach investors about land, scarcity, and long-term wealth creation.

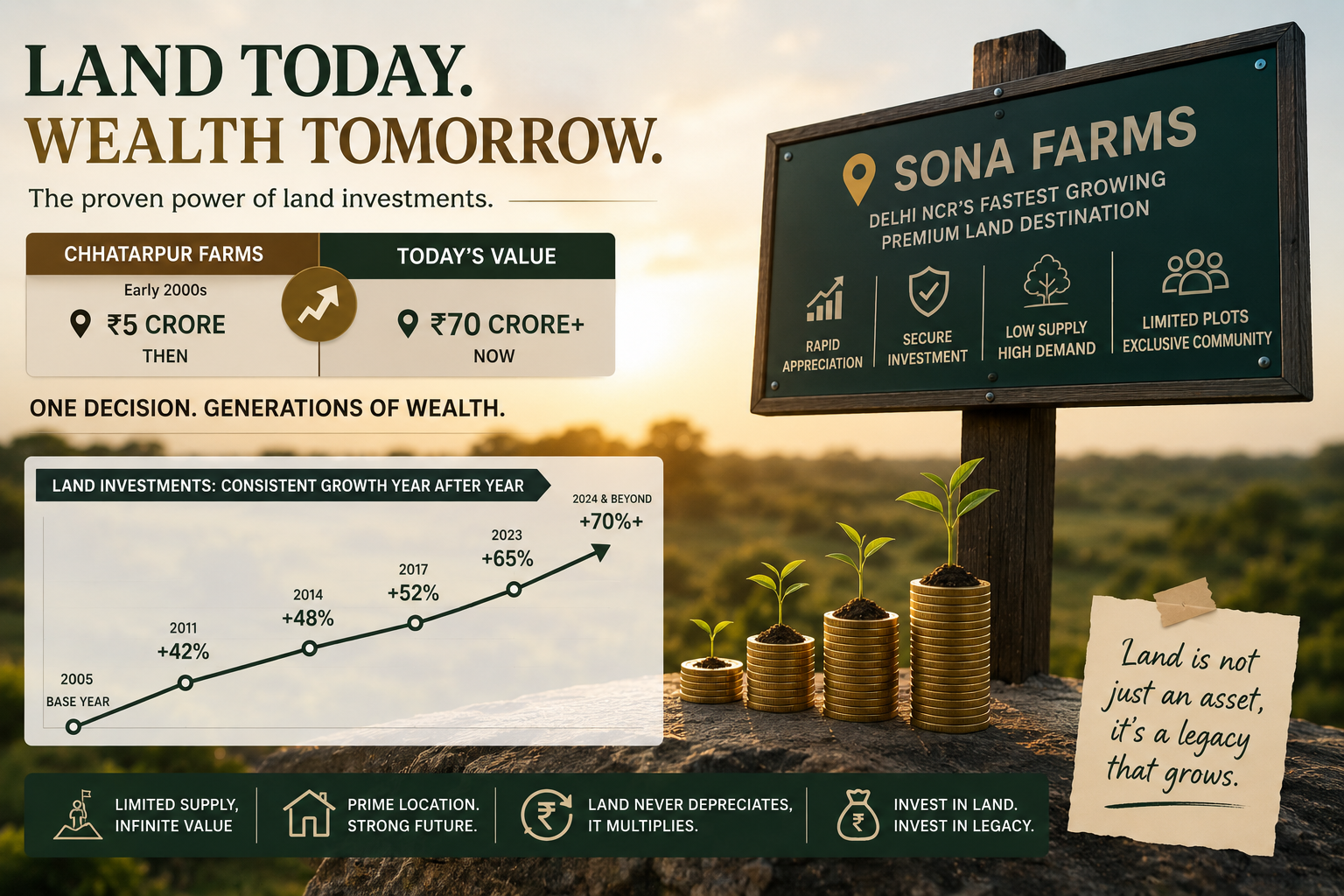

The ₹5 Crore Land Purchase That Became Worth ₹70 Crore

What the Story of DLF Chhatarpur Farms Reveals About Wealth Creation Through Premium Land Ownership

One short email. Stories you can use.

A free, occasional email from our editorial team with our latest features, explainers and reads. Unsubscribe any time — your email stays with us.