Why Perfume Ecommerce Is Exploding in 2026 — and How Niche Brands Are Quietly Beating the Designer Houses Online

Fragrance has become one of the fastest-growing categories in online beauty. Independent perfumers, TikTok discovery and sample-first commerce are rewriting a market that designer houses controlled for fifty years.

Fragrance is suddenly the loudest category in beauty. Circana's latest U.S. prestige beauty data shows fragrance growing faster than skincare, makeup or haircare for the fourth consecutive quarter, with online sales doing the heavy lifting. NPD's European tracker shows the same pattern across the U.K., France, Germany and Italy. The story matters because perfume — a category that retailers spent decades insisting could only be sold in person, on a paper blotter, by a trained consultant — has become one of the cleanest digital growth stories in consumer commerce.

A category that was supposed to be impossible online For most of the 2000s and 2010s, perfume ecommerce was treated as a structural laggard. The conventional wisdom held that nobody would spend £80 or more on a bottle they could not smell. That assumption broke for three reasons at once: a generation of shoppers who discover scent on TikTok rather than at a counter, the rise of low-friction discovery sets and decants, and a wave of independent perfumers willing to sell direct without ever opening a store.

TikTok turned fragrance into a content category #PerfumeTok now counts tens of billions of views. Creators like Jeremy Fragrance, Funmi Monet and a long tail of micro-reviewers have built genuine taste-making power, and the brands they champion routinely sell through within hours. Phlur's Missing Person became a generational case study — a niche launch that went from quiet release to permanent backorder almost entirely through unpaid creator content. Sol de Janeiro's body mists turned a Brazilian heritage brand into a global juggernaut on the back of TikTok-led discovery, and the playbook has since been copied by dozens of independents.

The niche houses are taking real share Le Labo, Byredo, Maison Francis Kurkdjian, Diptyque, Creed, Parfums de Marly, Xerjoff, Initio, Kilian and a long bench of smaller perfumers have moved from cult status to mainstream prestige in the West. LVMH's acquisition of Kurkdjian, Estée Lauder's earlier purchase of Le Labo and Byredo's sale to Puig were the early signals; the surge in independent niche brands launching directly to consumers is the second wave. Industry estimates put niche fragrance growth in the U.S. and Europe at two to three times the rate of mainstream designer fragrance over the past two years.

Sample-first commerce solved the smell problem The single biggest unlock for online fragrance has been the discovery set. Phlur, Dossier, DedCool, Snif, D.S. & Durga and most serious niche houses now ship low-cost sample vials or 2 ml decants that let shoppers try four to ten scents at home before committing to a full bottle. Scentbird and Scentbox have built subscription businesses around the same insight, and third-party decanting platforms like Scent Split and Decant House have turned sample commerce into its own ecosystem. The category finally has a try-before-you-buy model that works at internet scale.

Where shoppers are actually buying Sephora and Ulta dominate U.S. online prestige fragrance, with Amazon Premium Beauty taking a growing slice of the discovery and gifting market. In the U.K., The Perfume Shop, Boots, John Lewis and Cult Beauty split the bulk of online demand, while Bloom Perfumery and Les Senteurs anchor the niche end. Across continental Europe, Douglas, Notino, Sephora and Marionnaud handle most cross-border volume, with Jovoy in Paris and a handful of Italian and German specialists driving the high-end niche conversation. Brand-direct sites are growing fastest in absolute terms, but specialist retailers still own discovery.

Designer houses are responding — slowly Chanel, Dior, YSL, Tom Ford, Armani and Jo Malone London still hold the largest share of the global fragrance market, but their online growth rates are trailing the niche end of the category. The response has been to lean harder into limited editions, higher-concentration extraits, refillable formats and creator partnerships that look much more like the niche playbook than traditional luxury marketing. Dior's Sauvage refill program, Chanel's expansion of Les Exclusifs online and Tom Ford's Private Blend repositioning all reflect the same recognition: the rules have changed.

Refills, sustainability and the new luxury Refillable bottles have moved from sustainability talking point to genuine commercial driver. Mugler's Alien and Angel refills have been quietly profitable for years; Hermès, Chanel, Armani and a wave of niche houses including Floral Street and Akro have followed. For ecommerce, refills are doubly attractive — lower shipping weight, higher repeat-purchase frequency and a credible sustainability narrative that resonates with the same shoppers who buy resale fashion and clean beauty.

Fragrance is no longer a counter category that happens to have a website. It is an online-first discovery category with a physical finish — and the brands that understand the order of those words are the ones compounding fastest.

Gen Z is the engine Circana and Mintel both put Gen Z as the fastest-growing fragrance buyer cohort in the U.S. and U.K., with average per-person spend rising and bottle counts per shopper climbing. Younger buyers are layering scents, building wardrobes of three to seven fragrances rather than committing to a single signature, and treating perfume as part of a content-driven self-expression stack alongside skincare and makeup. That behaviour is exactly the demand profile online retail is built to serve.

What to watch next Expect more niche acquisitions by LVMH, Estée Lauder, Puig and Interparfums as the strategics race to lock down the next Le Labo. Expect Sephora and Douglas to keep expanding niche assortments online while quietly tightening the gate on undifferentiated mass launches. Expect refill-first formats to become table stakes in prestige. And expect TikTok Shop and Amazon Premium Beauty to keep pulling discovery downstream of the specialist retailers who built the category. For operators, the read-through is clear: fragrance ecommerce is no longer an emerging opportunity — it is one of the defining online beauty stories of the decade, and the window to build a credible niche brand inside it is open right now.

News Legacy maintains editorial independence. Some recommendations may contain affiliate links. We earn from qualifying purchases at no additional cost to you. Read our policy.

Read Next

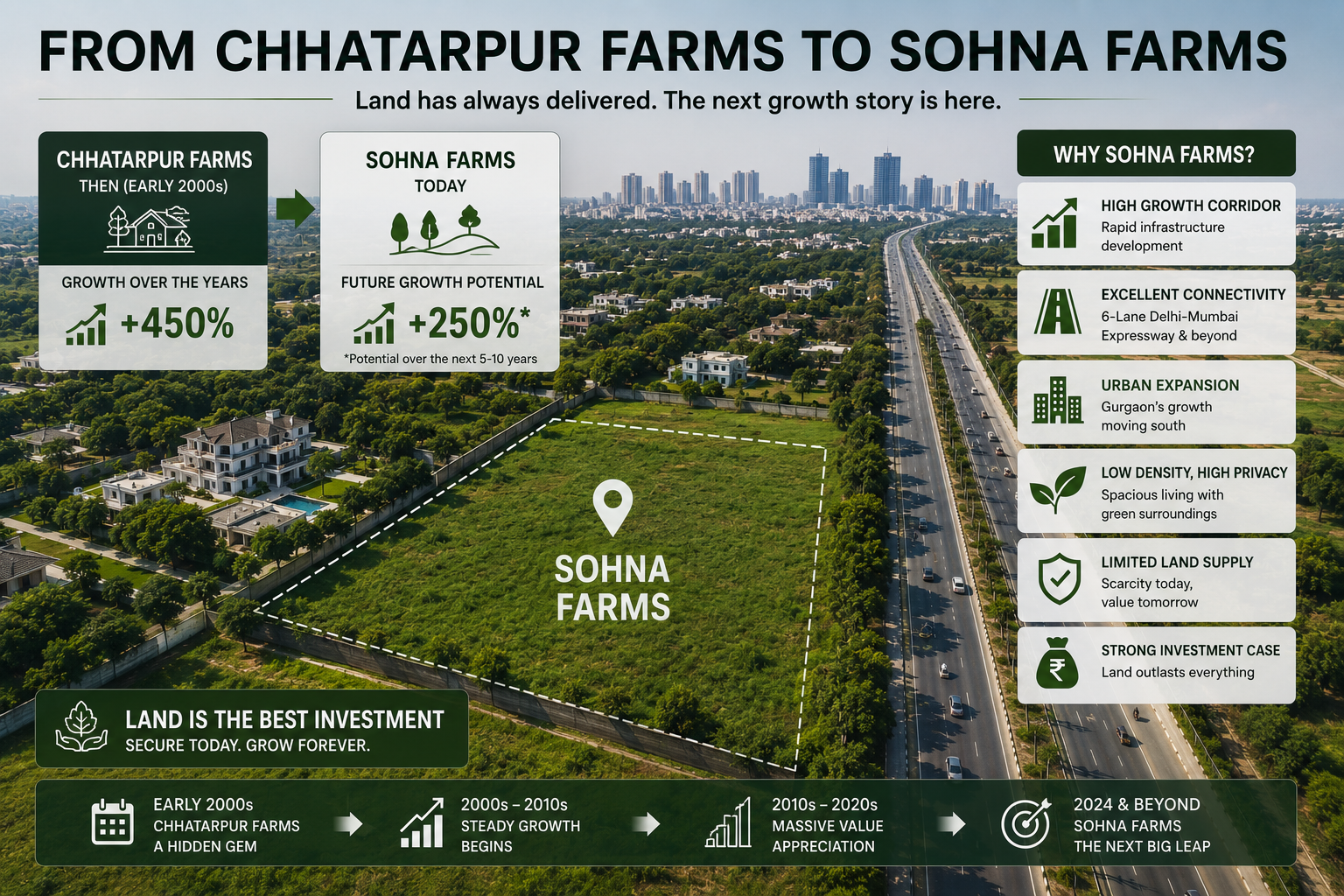

Is Sohna Really the Next Chhatarpur?

Three decades after Chhatarpur redrew South Delhi's map for space, privacy and exclusivity, a familiar pattern is now taking shape further south, and Sohna is where the smart money is beginning to look.

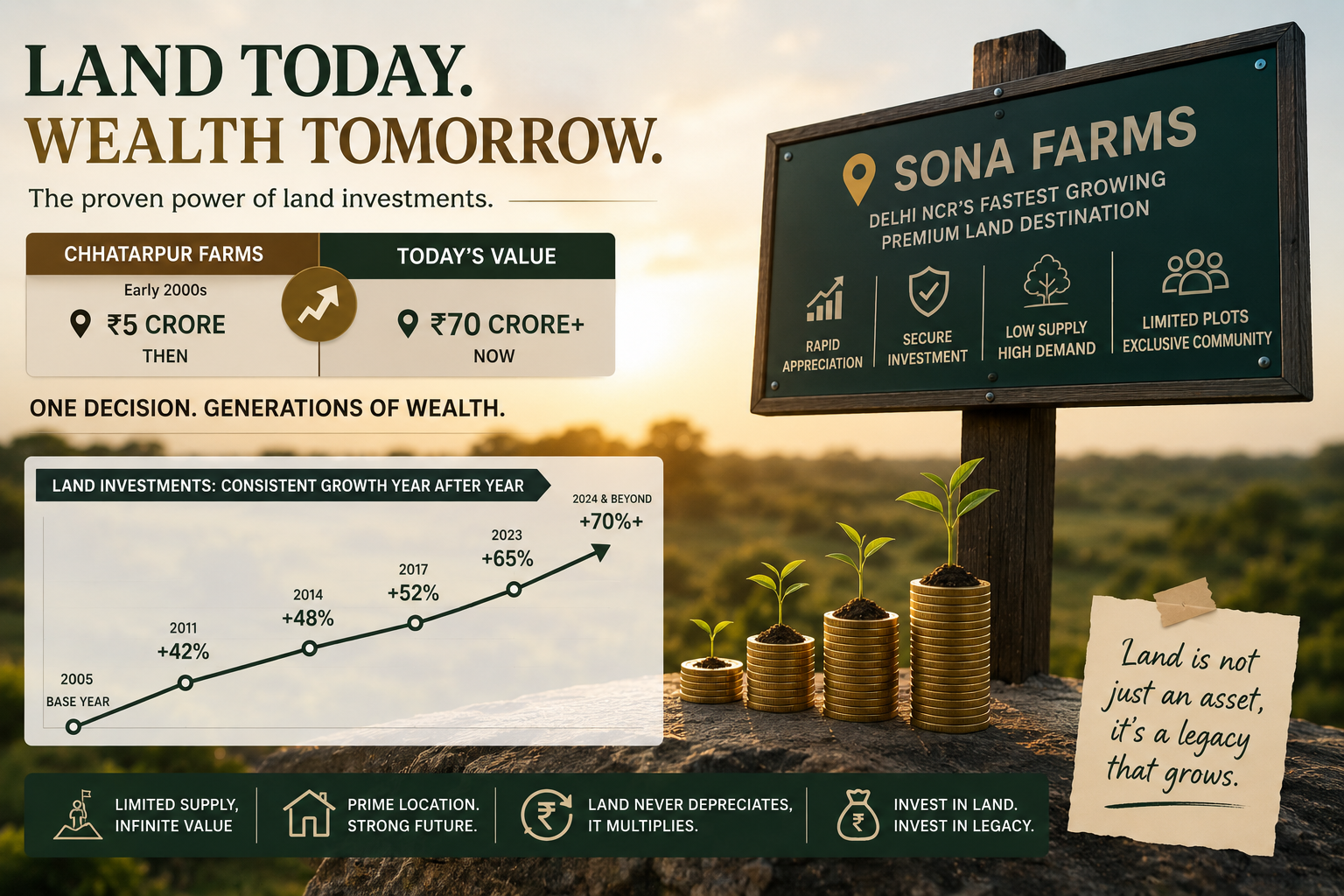

How Chhatarpur Farmhouses Created Multi-Crore Wealth for Early Buyers

What a quiet corner of South Delhi can teach investors about land, scarcity, and long-term wealth creation.

The ₹5 Crore Land Purchase That Became Worth ₹70 Crore

What the Story of DLF Chhatarpur Farms Reveals About Wealth Creation Through Premium Land Ownership

One short email. Stories you can use.

A free, occasional email from our editorial team with our latest features, explainers and reads. Unsubscribe any time — your email stays with us.