Quick Commerce's Uneasy Truce: From Blitzscaling to Sustainable Scrutiny

The rapid expansion of instantaneous delivery services in the UK has given way to a period of consolidation and strategic recalibration, as profitability rather than pure market share dictates the sector's future.

Even as Deliveroo riders weave through London's evening traffic, delivering meals and groceries, a more measured sentiment has settled over the quick commerce sector. The era of exponential growth, fuelled by venture capital and pandemic-driven demand, has transitioned into a colder assessment where the unit economics of rapid delivery are under intense scrutiny. This shift marks a pivotal moment for a segment that promised to redefine urban retail, now grappling with the complexities of long-term viability against a backdrop of inflationary pressures and evolving consumer habits.

The initial land grab saw companies like Getir and Gorillas burn through significant capital, offering aggressive discounts to capture market share. This strategy, while effective at building a user base quickly, proved unsustainable. Analysts widely report that many quick commerce operators were delivering at a loss, often absorbing significant portions of delivery fees to maintain competitiveness. The recent retrenchment, including market exits and operational scaling back, illustrates the industry's dawning recognition that convenience alone does not generate enduring value without a clear path to profitability.

The Legacy Retailer's Cautious Foothold

Traditional British supermarkets, initially wary of the instant delivery model's economics, have steadily built out their own rapid fulfilment capabilities. Tesco, for instance, has significantly expanded its Whoosh service, promising deliveries within an hour from a growing number of its larger stores. Sainsbury's similarly offers Chop Chop, leveraging its extensive store network to fulfil urgent orders. This approach mitigates the need for dedicated dark stores, instead utilising existing inventory and infrastructure, thereby reducing capital expenditure and operational complexity.

The integration strategy allows these incumbents to offer quick commerce as an extension of their core business, rather than a standalone venture. While not achieving the blistering delivery times initially marketed by pure-play quick commerce firms, their offerings are often more comprehensive in terms of product range and benefit from established supply chains. This provides a compelling alternative for customers who value reliability and breadth of choice alongside speed.

The quick commerce proposition, though enticing, must ultimately justify its premium through operational efficiency and genuine consumer need, not merely through the subsidisation of every transaction.

The Economic Imperative for Profitability

The macroeconomic climate in the UK has reinforced the imperative for quick commerce firms to demonstrate financial sustainability. Rising fuel prices, increased labour costs, and a general tightening of consumer spending have squeezed margins further. Customers, discerning in their expenditure, are increasingly evaluating the surcharge associated with instant delivery. While the convenience remains attractive, the willingness to pay several pounds for a fast delivery of a few items wanes when household budgets are under pressure.

For publicly listed entities like Deliveroo and Just Eat Takeaway.com, the emphasis from investors has shifted decisively from growth at any cost to a clear articulation of earnings potential. Both companies have faced calls to rationalise operations, cut unprofitable routes, and focus on core markets where they possess genuine competitive advantage. The focus on 'gross transaction value' as a primary metric is slowly being supplanted by 'adjusted EBITDA' and other measures of financial health.

Looking forward, successful quick commerce models will likely blend elements of both pure-play and integrated approaches. Partnerships, such as those between major grocers and third-party delivery platforms, offer a pathway to leverage established reach and logistical expertise. The future of quick commerce in the UK hinges not just on speed, but on the delicate balance of operational cost, customer value, and a robust economic model that can withstand market fluctuations.

The initial euphoria has given way to a sober reality, forcing a necessary evolution towards economically sound and strategically integrated services. The quick commerce promise endures, but its execution must adapt to the unforgiving demands of the balance sheet.

News Legacy maintains editorial independence. Some recommendations may contain affiliate links. We earn from qualifying purchases at no additional cost to you. Read our policy.

Read Next

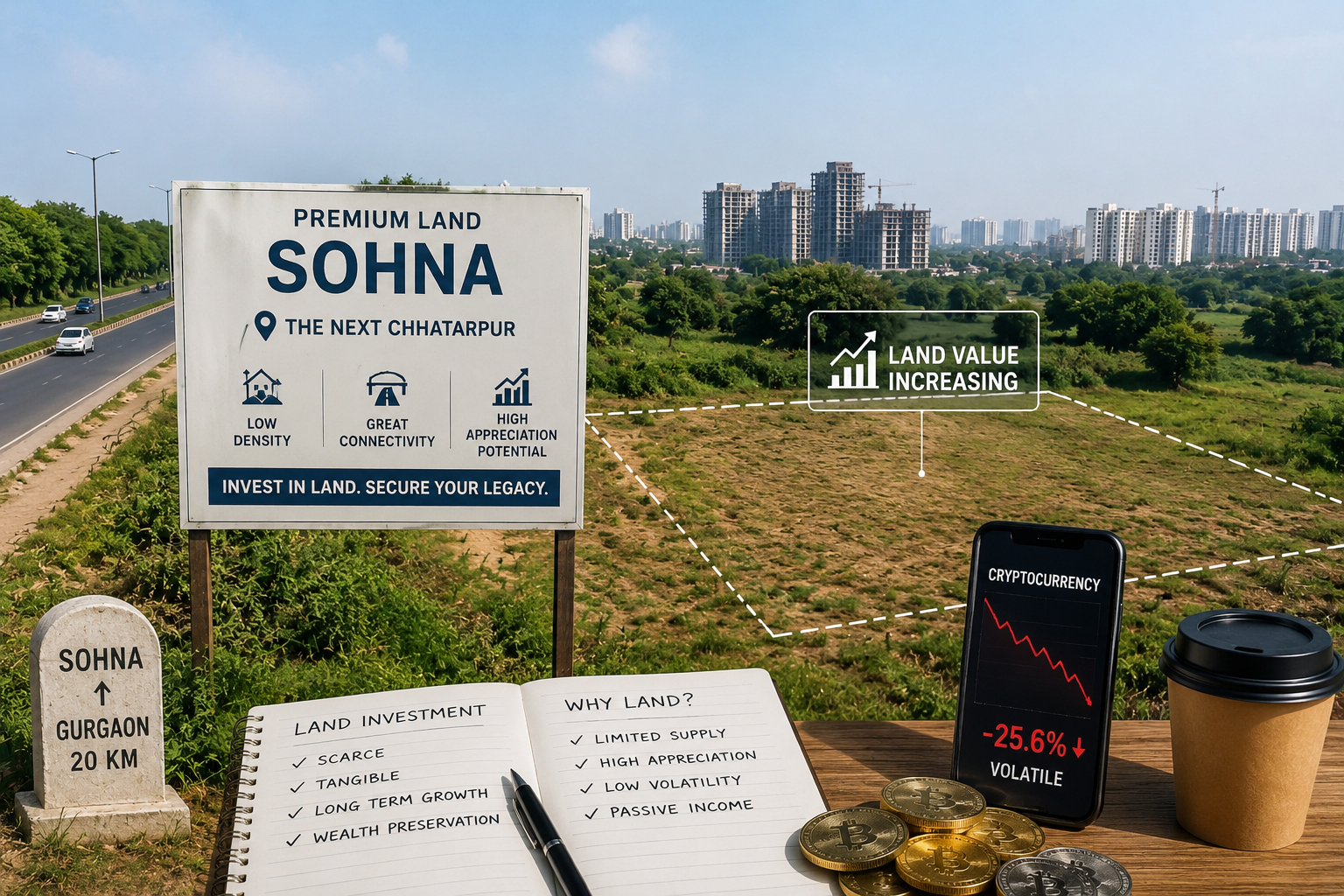

Is Sohna Really the Next Chhatarpur?

Three decades after Chhatarpur redrew South Delhi's map for space, privacy and exclusivity, a familiar pattern is now taking shape further south, and Sohna is where the smart money is beginning to look.

Why India's Wealthiest Families Still Buy Land

In an age of equities, private equity, startups and crypto, one asset class continues to attract the attention of India's wealthiest families, and the reason has less to do with returns than with scarcity.

The Top Ecommerce Niches Quietly Winning the U.S., U.K. and European Markets in 2026

Beauty, athleisure, wellness, pet and resale are no longer trends — they are the operating cores of online retail across the West. Here is where the money is actually moving.

One short email. Stories you can use.

A free, occasional email from our editorial team with our latest features, explainers and reads. Unsubscribe any time — your email stays with us.