The High Street's Unseen Advantage: How Structural Costs Buffer Against DTC Onslaughts

While direct-to-consumer brands once heralded the demise of traditional retail, a closer examination of the UK market reveals how legacy infrastructure and cost structures now offer an unexpected bulwark.

In the labyrinthine aisles of a Tesco Extra, amidst the familiar glow of chilled cabinets and promotional end-caps, the sheer scale of the operation becomes evident. This extensive physical footprint, once deemed an anchor weighing down traditional retailers, is now proving to be a surprising asset in the face of direct-to-consumer (DTC) challengers. The narrative of DTC brands disrupting established retail models has long dominated industry discourse, yet the reality on the ground in the UK suggests a more nuanced interaction.

For years, DTC brands leveraged agility, personalised marketing, and a direct relationship with consumers to undercut larger incumbents. Warby Parker's disruption of eyewear or Glossier's ascent in beauty were held up as prime examples. However, the cost of customer acquisition has escalated dramatically. With digital advertising rates driven up by competition and privacy changes, the once-efficient direct funnel has become increasingly expensive to maintain. Many celebrated DTC brands are now finding profitability elusive, even at significant revenue scales.

The Infrastructure Premium

Traditional UK retailers like Marks & Spencer, Next, and even the grocery giants like Sainsbury's, possess deeply embedded distribution networks, often including hundreds of physical stores, dedicated delivery fleets, and robust supply chain infrastructure. These assets, built over decades and amortised over vast turnovers, represent a substantial barrier to entry for smaller, newer entrants. For instance, the capital expenditure required to replicate the logistical capacity of an Ocado or a Deliveroo is staggering, far exceeding the typical venture capital rounds secured by most DTC start-ups.

The cost of 'last mile' delivery, particularly in a geographically constrained and densely populated market like the UK, consumes a significant portion of a product's margin. While DTC brands originally absorbed these costs to build market share, the continuous erosion of profitability has forced a recalculation. Many are finding that outsourcing logistics adds another layer of expense, further squeezing their already thin margins.

The market was perhaps too swift to declare the storefront obsolete; its underlying economic efficiencies were simply re-evaluated.

Furthermore, the sheer purchasing power of established players allows for economies of scale that elude smaller brands. Whether negotiating container freight from Asia or securing prime advertising slots, a company like ASOS or even a major supermarket can command better terms than a niche online seller. This contributes directly to a healthier gross margin, providing a buffer against unexpected cost increases or aggressive pricing from competitors.

Evolving Consumer Expectations and Trust

UK consumer behaviour also plays a crucial role. While online shopping has become ubiquitous, particularly since 2020, there remains a strong preference for immediacy and the ability to return goods easily. Physical stores provide both. The ability to click-and-collect an item from a local branch, or to test a product before purchase, offers a tangible advantage that pure-play online brands struggle to replicate without significant investment in showrooms or partnerships. Trust, too, is a powerful currency. Brands like John Lewis or Boots have cultivated decades of customer loyalty, a form of intangible asset that takes years, if not generations, to build and cannot be bought outright.

The strategic pivot by many successful pure-play online retailers towards incorporating physical retail demonstrates this shift. They are implicitly acknowledging that an omnichannel approach, rather than a purely digital one, is necessary for sustained growth and profitability. The structural costs that once characterised 'old retail' are now, somewhat ironically, underpinning much of its enduring strength against a new generation of challengers.

News Legacy maintains editorial independence. Some recommendations may contain affiliate links. We earn from qualifying purchases at no additional cost to you. Read our policy.

Read Next

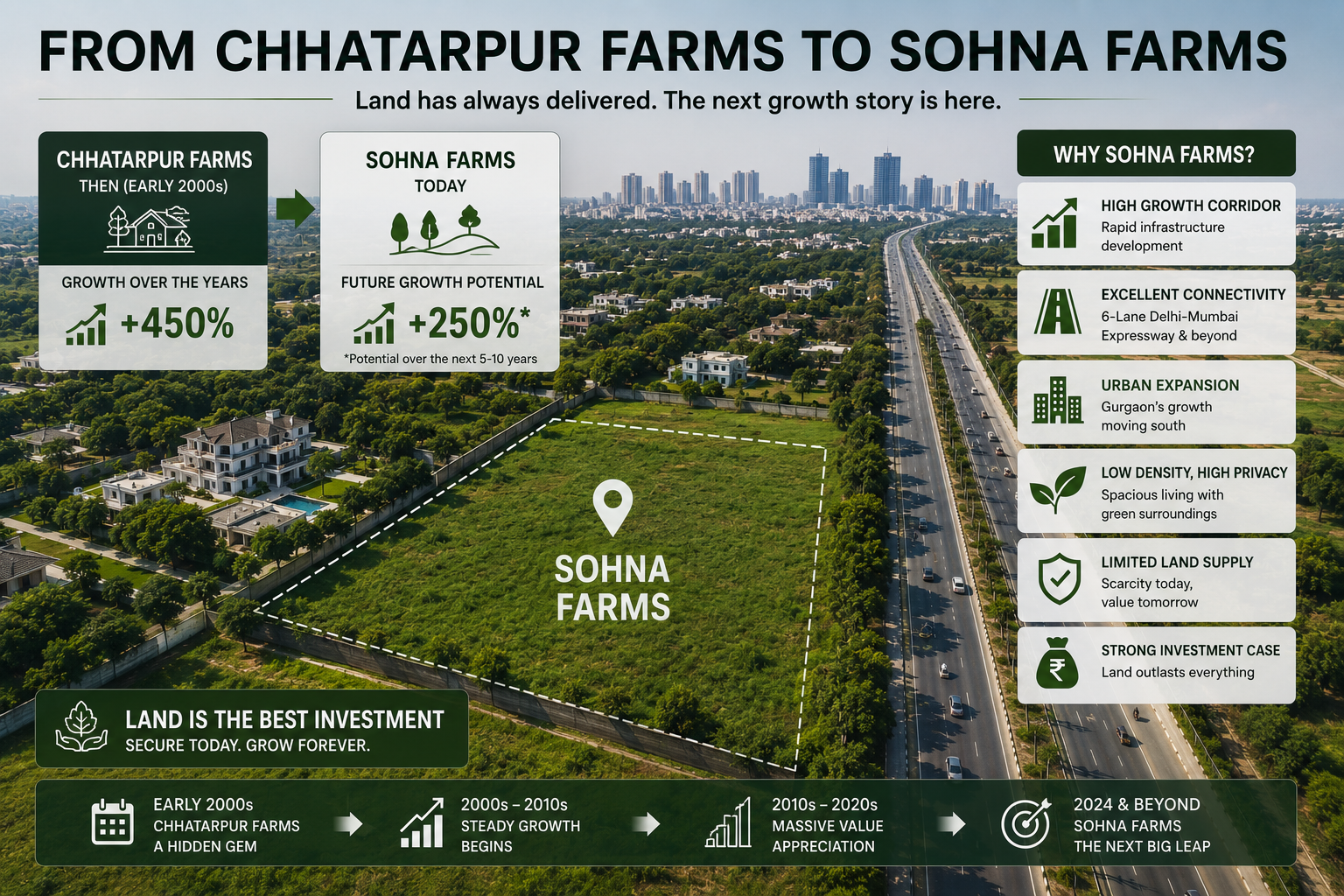

Is Sohna Really the Next Chhatarpur?

Three decades after Chhatarpur redrew South Delhi's map for space, privacy and exclusivity, a familiar pattern is now taking shape further south, and Sohna is where the smart money is beginning to look.

How Chhatarpur Farmhouses Created Multi-Crore Wealth for Early Buyers

What a quiet corner of South Delhi can teach investors about land, scarcity, and long-term wealth creation.

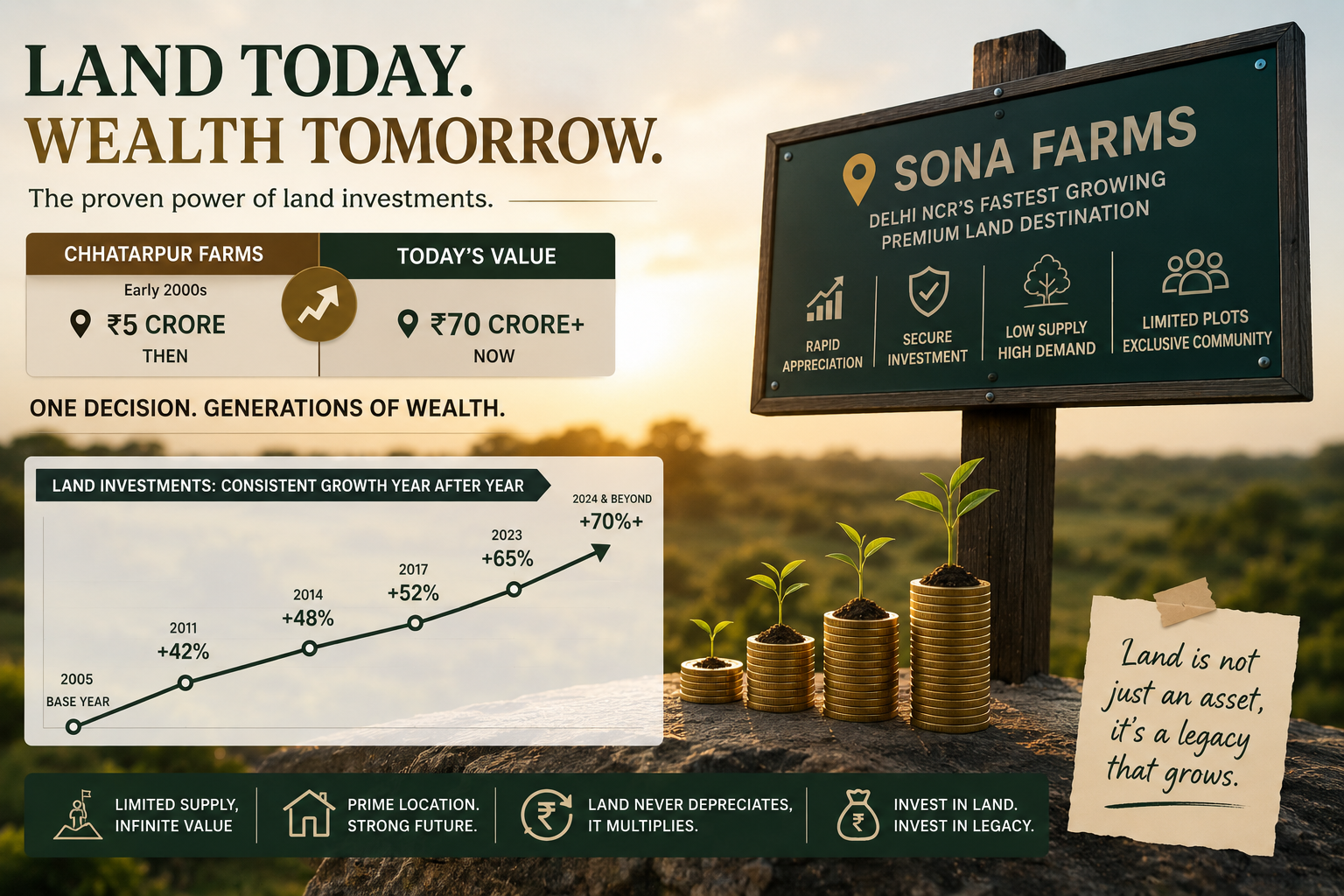

The ₹5 Crore Land Purchase That Became Worth ₹70 Crore

What the Story of DLF Chhatarpur Farms Reveals About Wealth Creation Through Premium Land Ownership

One short email. Stories you can use.

A free, occasional email from our editorial team with our latest features, explainers and reads. Unsubscribe any time — your email stays with us.