The Price of Proximity: Quick Commerce Grapples with Profitability in the UK

Despite robust consumer demand for rapid delivery, the quick commerce sector in the United Kingdom faces an increasingly acute challenge in translating convenience into sustainable financial returns. Operational complexities and intensifying competition are forcing a strategic recalibration.

Even as a Just Eat rider zips past a Tesco Express in central London, laden with groceries for a nearby customer, the underlying economics of quick commerce in the UK remain fiercely debated. While consumer appetite for instant gratification has undeniably surged, driven by pandemic-era habits, the pathway to consistent profitability for these rapid delivery platforms is proving narrower and more complex than initially forecast.

The model, predicated on delivering a small basket of goods within minutes, demands significant investment in localised dark stores or partnerships with existing retailers, alongside a substantial fleet of couriers. This high fixed-cost base, coupled with the pressure to offer competitive pricing and free delivery bundles, has often led to operating losses, even as gross transaction value climbs.

The Evolving Landscape of Partnership and Integration

Initially, many quick commerce players, such as Getir and Gorillas, pursued a vertically integrated model, owning both the inventory and the delivery infrastructure. However, the consolidation seen in the sector – with Gorillas acquired by Getir, and numerous smaller players withdrawing – suggests a shift. The increasing prevalence of partnerships, where established grocers like Sainsbury's and Morrisons leverage platforms like Deliveroo or Uber Eats for their 'rapid' offerings, points to a recognition that asset-light models may be more sustainable. Tesco, for instance, has significantly expanded its Whoosh rapid delivery service, leveraging its extensive store network.

Retailers are effectively outsourcing the complex logistics of last-mile, on-demand delivery, allowing them to tap into a new revenue stream without the full capital expenditure. For the delivery platforms, such partnerships provide a more stable, higher-volume pipeline of orders, diversifying their revenue beyond restaurant meals and reducing the financial burden of managing their own inventory.

The quick commerce proposition is compelling for consumers, yet the challenge for operators lies in capturing sufficient margin to cover the intensive logistical overheads without alienating a price-sensitive market.

The Quest for Operational Efficiency and Market Rationalisation

Beyond partnerships, the drive for efficiency is paramount. This involves optimising routing algorithms, implementing real-time inventory management in dark stores, and carefully calibrating delivery zones to minimise courier idle time. The UK market, while dense, presents its own unique challenges, from urban congestion to fluctuating demand patterns tied to weather and local events.

The capital expenditure required to establish and maintain a quick commerce footprint is substantial. Investors, once eager to fund rapid expansion, are now scrutinising unit economics more closely. This shift in sentiment has likely contributed to the more measured growth strategies and the consolidations witnessed across the sector. Companies are prioritising sustained profitability over sheer market share, a pivot that suggests a more mature, if less frenetic, phase for rapid delivery in Britain.

Looking forward, the sector is likely to see further innovation in technology and greater integration with broader retail strategies. The battle for the convenience shopper's pound will not diminish, but the victors will be those who can blend technological prowess with an astute understanding of operational costs and consumer willingness to pay for speed.

News Legacy maintains editorial independence. Some recommendations may contain affiliate links. We earn from qualifying purchases at no additional cost to you. Read our policy.

Read Next

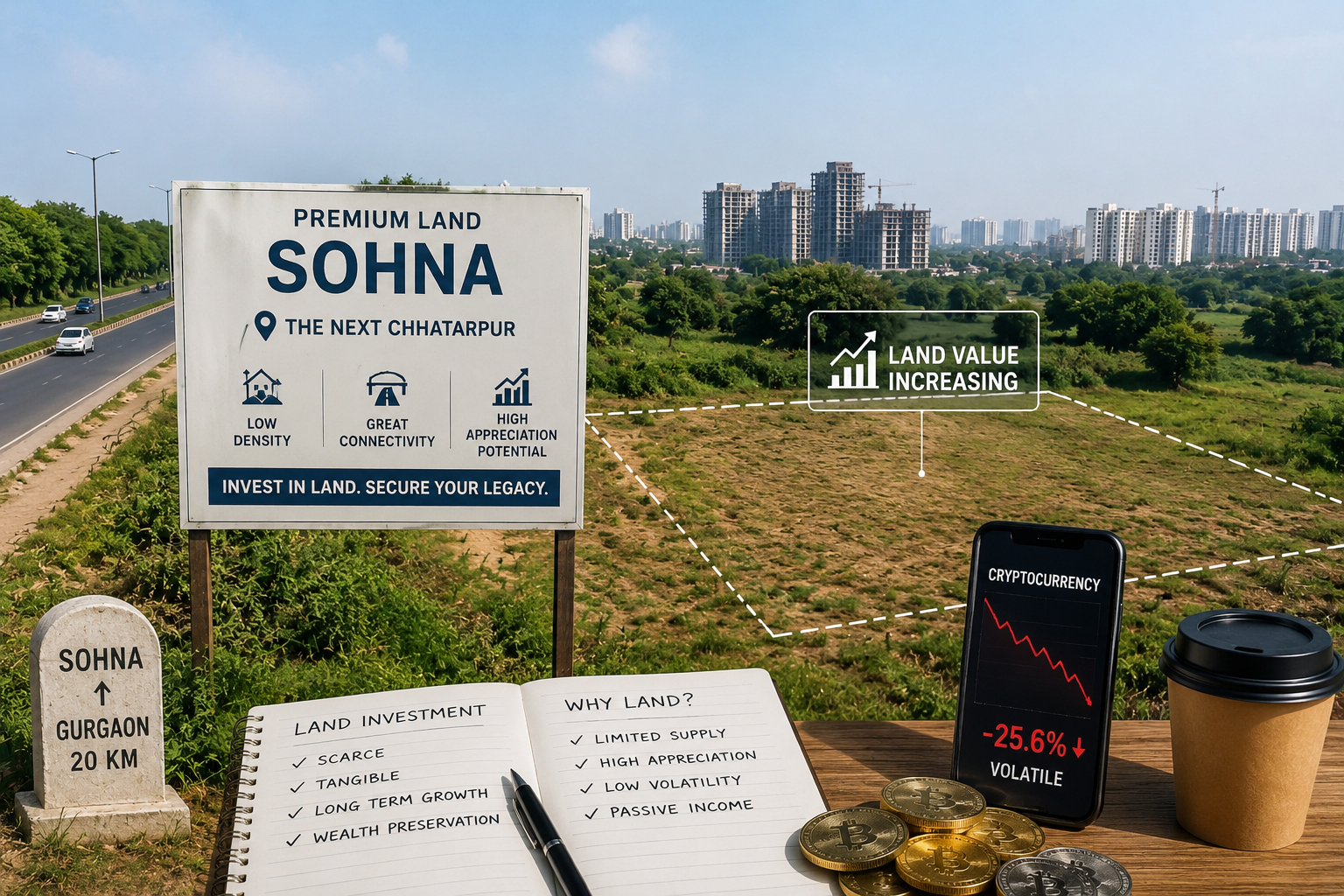

Is Sohna Really the Next Chhatarpur?

Three decades after Chhatarpur redrew South Delhi's map for space, privacy and exclusivity, a familiar pattern is now taking shape further south, and Sohna is where the smart money is beginning to look.

Why India's Wealthiest Families Still Buy Land

In an age of equities, private equity, startups and crypto, one asset class continues to attract the attention of India's wealthiest families, and the reason has less to do with returns than with scarcity.

The Top Ecommerce Niches Quietly Winning the U.S., U.K. and European Markets in 2026

Beauty, athleisure, wellness, pet and resale are no longer trends — they are the operating cores of online retail across the West. Here is where the money is actually moving.

One short email. Stories you can use.

A free, occasional email from our editorial team with our latest features, explainers and reads. Unsubscribe any time — your email stays with us.